Internet Explorer is not supported by this website. For a better viewing experience, upgrade to Microsoft Edge.

Internet Explorer is not supported by this website. For a better viewing experience, upgrade to Microsoft Edge.

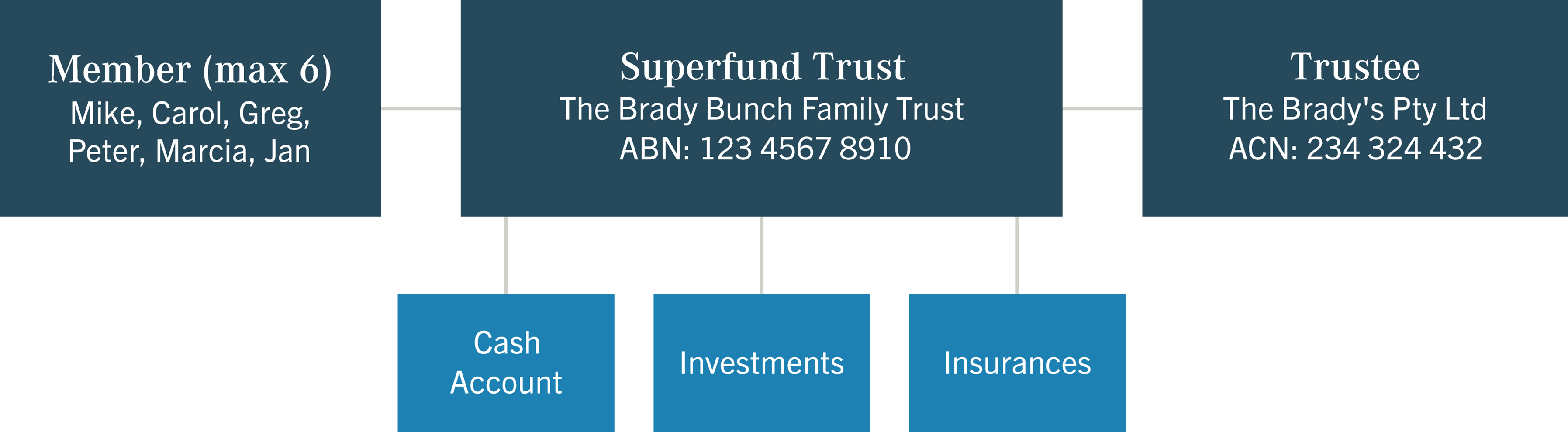

Self-Managed Superannuation is one of the most popular retirement savings vehicles in Australia.

SMSF’s now control over 25% of money held in the entire Australian superannuation market with over 590,000 funds holding more than $730 billion in total assets (as at 30/6/2020). The average fund size is now greater than $1.3million.

Setting up an SMSF can be exciting. It allows you to control and have total transparency of your superannuation and pension funds and it is the only vehicle that allows partners and multi generations to aggregate their savings and investments to provide a desired income for retirement. Furthermore, it is the only superannuation structure that allows members to borrow for investment or acquire directly held property.

The decision to establish and run a SMSF is not one to be taken lightly. There are set up and ongoing costs to be considered, regulations to abide by, ongoing tax and audit responsibilities as well as ongoing investment decisions and trustee obligations.

Before considering setting up an SMSF we advise that you first consider your “intent”.

That is, what are your longer term goals and objectives and what is it you are trying to achieve? Is an SMSF right for you or are you best to retain your existing superannuation fund?

At all times it is recommended you discuss your objectives and seek advice from specialist SMSF financial advisers and accountants.

Control

The trustees (usually the members) determine the investment strategy and can select specific investments of the fund. This provides an investor with control over the investment portfolio, including member- directed investments.

Flexibility

SMSFs are an extremely flexible superannuation savings vehicle. SMSFs can receive contributions and rollovers whilst also being able to pay retirement benefits in a lump sum or pension. Future generations of a person’s family can use the fund to save for retirement.

Full Knowledge of Investments Held

A SMSF enables members to control where funds are placed, and consequently a greater knowledge and transparency of the current state of the fund investments.

Diversification

Being a trustee of a SMSF gives you the control over what investments you have for your fund. It also allows you to invest in assets that may not be available in retail and industry super funds such as various direct shares, direct property and initial public offerings (IPOs).

Borrow to Invest

Unlike other Superannuation funds an SMSF is able to borrow to invest in a “single acquirable asset” (e.g. Direct property). This may be relevant to persons that need to borrow to fast track or catch up on their retirement planning or to small business owners that want to use their SMSF to buy their business premises.

Estate Planning

One of the advantages of SMSFs is the level of control and flexibility they offer members due to the fact that they control the fund. In terms of estate planning this control and flexibility can be of great advantage as it can allow a member to determine:

Tax Planning

A SMSF has more control on how it manages its tax liabilities. For instance it can delay payment of its contributions tax liability until after the completion of the annual SMSF tax return and as such funds can be fully invested in the meantime.

Good for Substantial Amounts

Those with substantial assets (at the least $500,000) stand to gain most by establishing and managing a SMSF. There are two main reasons:

Obligations of Trustee

As a member and therefore Trustee you are bound by law to responsibly manage the superannuation fund for the members. Non- compliance can result in penalties. There are administrative and compliance tasks which must be fulfilled by the trustees of the fund. These tasks are time consuming. Trustees need to keep up to date with tax and super legislation, or utilise the services of professional advisors such as specialist financial planners and accountants.

Costs

Costs can be expensive relative to the fund size. A retail/ industry fund may be cheaper depending on the asset level and how assets are invested. Also, where the fund’s assets are invested into a retail managed fund, a doubling up of expenses can eventuate. Accounting and audit fees are payable and management fees are also charged by the fund manager.

Fund Performance

A professional fund manager with considerable investment expertise and resources should outperform an amateur investor over the medium to long term. That said you can utilize the services of professional fund managers within your SMSF.

Lack of Diversification

There is a risk trustees will not give due consideration to diversification and, accordingly medium- to long-term returns may be lower than those achieved by a retail fund.

A SMSF may be suitable for people who:

A SMSF may not be suitable for people who:

A SMSF has four main components that need to be organised every year to make sure that the fund is complying with the ATO standards. As a trustee you have the discretion to outsource these components to professionals and in most cases you will find that it is a better option to do this. Firstly, because it reduces the risk of the fund becoming non-compliant, secondly because it reduces the amount of time you are required to spend controlling the fund.

The four components are:

A SMSF has investment restrictions. The superannuation law doesn’t state exactly what a fund can and can’t invest in. However, it does restrict some investment practices.

The investment restrictions aim to protect fund members by making sure fund assets are not overly exposed to undue risk (e.g. the possible risk of an associated business failing).

Furthermore, SMSFs must make investment decisions with the primary purpose of generating retirement benefits for members. SMSFs are not to provide current day support to members, employer-sponsors or their associates.

Failure to comply with SMSF investment rules could result in trustees being fined and/or the fund losing its compliance status. SMSF trustees are also prohibited from lending money, or providing financial assistance from the fund, to a member or a member’s relative. The use of a fund asset by a member or a member’s relative for no cost (or as a guarantee to secure a personal loan) would be in breach of this investment restriction.A SMSF may borrow to invest. The borrowing must have the following features:

Below is a typical structure using borrowed funds to buy a residential property via an SMSF. Note, there is a separate trust in addition to your SMSF called a “Security Trust” that holds the property until the loan is paid.

How does my SMSF purchase a property?

The SMSF chooses the asset in the ordinary manner. Property must be purchased in a commercial ‘arm’s length’ manner. Non-Residential property can be purchased from related vendors so long as it is to be used for business purposes. The SMSF obtains the loan approval. All associated costs of acquisition including payment of the deposit are paid in the ordinary manner by the SMSF. On completion of the purchase, the SMSF manages the property in the ordinary manner.

Can fund members occupy the property?

No. If fund members or related persons occupy the property, the ‘in-house asset rule’ will have been breached. The exception is where the property is commercial and the member’s business/ company rents the property from the SMSF on a commercial basis. (i.e. Market rental)

What other restrictions apply?

The SMSF must comply with all regulations applying to superannuation funds. SMSFs must ensure that the level of investment in any asset class is consistent with its investment strategy. This includes diversification, liquidity and maximising member returns.

The government has also made it clear that super funds investing in these types of investments must have appropriate risk management measures in place and must understand the risks of the investment.

Who pays what and when?

As beneficial owner of the property and the borrower of the loan, the SMSF is responsible for paying all usual costs that are expected if an asset was bought outside of super. These costs can include: council rates, water rates, land tax, interest costs, loan repayments, lenders fees, repairs, property management costs, insurance premiums and associated costs if listed investments are purchased.Disclaimer: This article contains information that is general in nature. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decisions based on this information.

Navigate Financial Group Pty Ltd as trustee for NFG Unit Trust (ABN 91 414 170 076) trading as Navigate Financial Group is an authorised representative and credit representative of AMP Financial Planning Pty Limited (ABN 89 051 208 327), Australian Financial Services Licensee and Australian Credit License No. 232706. This website contains information that is general in nature. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decisions based on this information.

Copyright © 2022 All Rights Reserved | Navigate Financial Group